Are Canadians saving enough for retirement? What can contributions to retirement plans tell us about saving levels?

In a June commentary for the C.D. Howe Institute, Malcolm Hamilton shows why the household saving rate doesn’t answer the question whether or not Canadians are saving too little for retirement. In his own paper for the Canadian Centre for Policy Alternatives, Michael Wolfson agrees, arguing that the real question is how much individuals can afford to spend on consumption after retirement, as compared to prior to entering retirement. To evaluate this, Wolfson argues, sophisticated modelling taking into account the complexity and diversity of individual experiences over a lifetime is necessary, not simple reference to averages and aggregates.

As Hamilton demonstrates, Statistics Canada’s National Accounts data on the household saving rate combine saving (typically working households building equity in their home or saving for retirement) and “dissaving” (typically older households that have begun to receive a pension, or are drawing down on their accumulated retirement savings). The household saving rate is an aggregate of these competing forces; because it doesn’t separate saving from dissaving, it’s not an accurate picture of whether working Canadians are saving adequately for retirement.

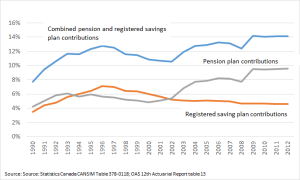

To illustrate the point, Hamilton shows that between 1990 and 2012, the household saving rate (net saving as a share of disposable income) fell from 11.7% to 5.2%. At the same time, retirement contributions as a share of employment earnings rose from 7.7% in 1990 to 14.1% in 2012. Regardless of the falling household saving rate, Hamilton argues, contributions going toward retirement nearly doubled as a share of earnings between 1990 and 2012.

It’s true that between 1990 and 2012, combined contributions to workplace pension plans and individual registered savings plans (like RRSPs) nearly doubled relative to earnings. But this resulted from an increase in pension contributions, offsetting a drop in saving plan contributions (figure 1).

Figure 1: Pension and Individual Retirement Savings Plan Contributions as a Share of Employment Earnings, Canada, 1990-2012

As interest rates fell after 2001 and defined-benefit plans became more expensive, contributions rose. At the same time, the level of contributions to individual saving plans trended downwards, as the baby-boomer cohort reached retirement age.

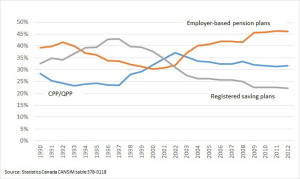

Measured as a share of contributions to all plans, workplace pension contributions have been rising, and individual saving plans have fallen (figure 2). Contributions to the Canada/Quebec Pension Plans rose between 1997 and 2003 as part of the federal government’s overhaul, and have trended slightly downwards since then.

Figure 2: Pension, CPP/QPP, and Individual Retirement Savings Plan Contributions as a Share of Total Plan Contributions, Canada, 1990-2012

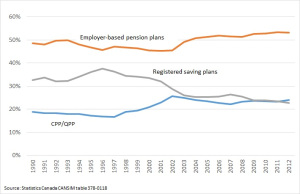

The trend is not significantly altered when investment income is added to contributions (figure 3).

Figure 3: Pension and Individual Retirement Savings Plan Inflows (Contributions + Investment Income) as a Share of Total Plan Inflows, Canada, 1990-2012

What this means is that the apparent increase in retirement contributions was mostly due to the rise in workplace pension plans; individual saving plan contributions fell as a share of employment earnings and as a share of all contributions to retirement saving vehicles.

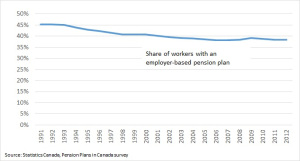

This is a problem, because a shrinking minority of workers in Canada are covered by a workplace pension plan (figure 4).

Figure 4: Pension Plan Coverage in Canada

Rising pension plan contributions may be boosting overall household retirement contributions, but they’re coming from a dwindling minority of workers fortunate to have a pension at work. For the vast majority left to rely on individual retirement savings plans like RRSPs and TFSAs, the trends in contributions are not encouraging.

photo credit: The Old Folks via photopin(license)

Leave a Reply